What are the biggest cannabis vape trends in 2026?

Cannabis vape is an $8 billion category, and in 2026, it is changing faster than at almost any point in its history. The five biggest cannabis vape trends reshaping the market right now are:

- Vape has surpassed flower as the top-selling category in California and Washington

- Disposables have overtaken cartridges as the leading format for the first time

- The 2-gram disposable is the fastest-growing format size, doubling its share in two years

- Live resin and premium oil types are gaining share at the expense of distillate

- Brand consolidation is accelerating in mature markets while new markets are still expanding

Vape’s share of total cannabis retail has held steady at 26% over the past year, up 6% in total dollars to $8 billion. By the top-line measure, vape looks stable. Beneath that headline, the composition of the category is shifting faster than it has in years.

1. Is vape bigger than flower in cannabis?

The short answer: Nationally, no — flower is still the largest cannabis category at 40% of retail versus vape’s 26%. But in California and Washington, vape has already overtaken flower as the top-selling category as of late 2025 and early 2026.

Nationally, flower still leads at 40% of cannabis retail versus vape’s 26%, and that ranking is not close to flipping at the national level. The movement is happening at the state level.

In May 2026, measured as share of each state’s total cannabis market:

-

Washington: vape holds 32% of the market versus flower’s 26% — a 5.8-point lead, the clearest vape-first market in the country

-

California: vape at 31% versus flower’s 30% — vape leads by just 1.4 percentage points, the most recently tipped market and still close

-

Arizona: vape at 31%, flower at 33% — just 2 percentage points apart and closing

-

New York: vape at 26%, flower at 32% — a 6-point gap

-

Illinois, New Jersey, Ohio, Massachusetts, and Colorado: flower leads by 11 to 18 percentage points — vape is growing but the gap remains meaningful

-

Florida: flower at nearly 50% of the market versus vape’s 23% — a 26-point gap reflecting a heavily flower-oriented consumer base

-

Michigan: an outlier in a class of its own — flower holds nearly 60% of the market versus vape’s 14%, a 46-point gap that stands apart from every other major market on this list

California’s crossover is the most significant data point. It only occurred in late 2025, which means averaging over a full 12-month window would obscure it entirely. Tow of the most mature markets in the country have tipped to vape-first. In cannabis market history, that is usually where national trends begin.

2. Disposable vapes have overtaken cartridges — but the split varies widely by state

The short answer: Disposable vapes crossed 50% of U.S. vape market share for the first time in April 2026 and reached 51% in May 2026, making them the majority format nationally for the first time in cannabis history.

For most of cannabis’s modern era, the vape cartridge was the default format. That is no longer true. Over the past 12 months, disposable vapes grew 41% to $3.8 billion while vape cartridges fell 14% to $4.1 billion. However, the past-year figures understate how decisively this has flipped, because the crossover only happened recently.

The latest data tells the real story: disposables made up 42.9% of vape dollars in June 2025, climbed almost every month, crossed 50% in April 2026, and reached 51.1% in May 2026.

What is driving the shift to disposable vapes? Three factors: consumer preference for convenience and portability, aggressive pricing in the disposable segment, and the rapid rise of large-format 2-gram SKUs that offer strong perceived value at a higher price point.

Important to note that even with the national cross-over, there significant state-by-state variation. In May 2026:

- Highest disposable share: Arizona (79%), New York (66%), Michigan (64%)

- Lowest disposable share among major markets: Florida (32%), Pennsylvania (39%), California (46%). Worth noting that Florida and Pennsylvania are both med markets.

The “majority format” milestone is a national average stretched across markets that range from heavily disposable to heavily cartridge, shaped by local consumer preferences, pricing dynamics, and which brands are competing on shelf in each state.

Disposables are still growing, but there is some deceleration in that growth as the format matures. How much further disposables extend their lead will depend largely on whether cartridge-heavy holdout states eventually follow the pattern set by Arizona and New York.

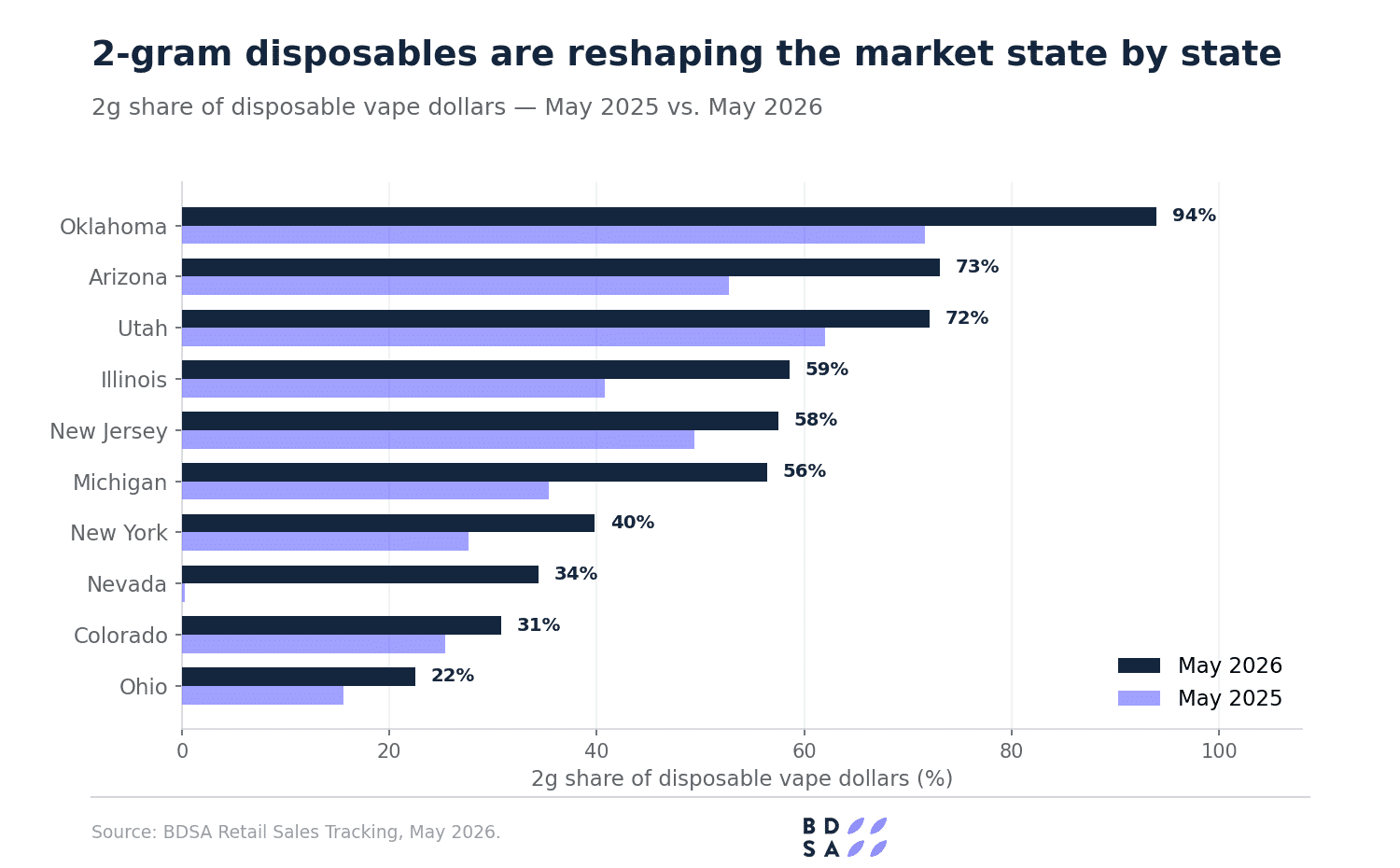

3. The 2-gram disposable is the fastest-growing format in cannabis vape

The short answer: 2-gram disposables have grown from 16% to 35% of all disposable vape dollars in just two years, more than doubling their share nationally.

Within the broader disposable surge, the 2-gram size is doing most of the work. Two years ago, 2-gram disposables accounted for roughly 16% of disposable vape dollars nationally. By May 2026, that share had reached 35% — more than doubling in 24 months. Gains have come almost entirely at the expense of smaller formats like 300mg and 500mg. The 1-gram has held steady at around 53% of disposable dollars, meaning the format battle is playing out at the smaller end of the size spectrum rather than displacing the 1g standard.

Which states have the highest 2-gram disposable share? As of May 2026:

- Oklahoma: 94% of disposable vape dollars

- Arizona: 73%

- Utah: 72%

- Illinois: 59% (up from 41% a year ago)

- Nevada: 34% (up from under 1% a year ago — the sharpest state-level shift in the data)

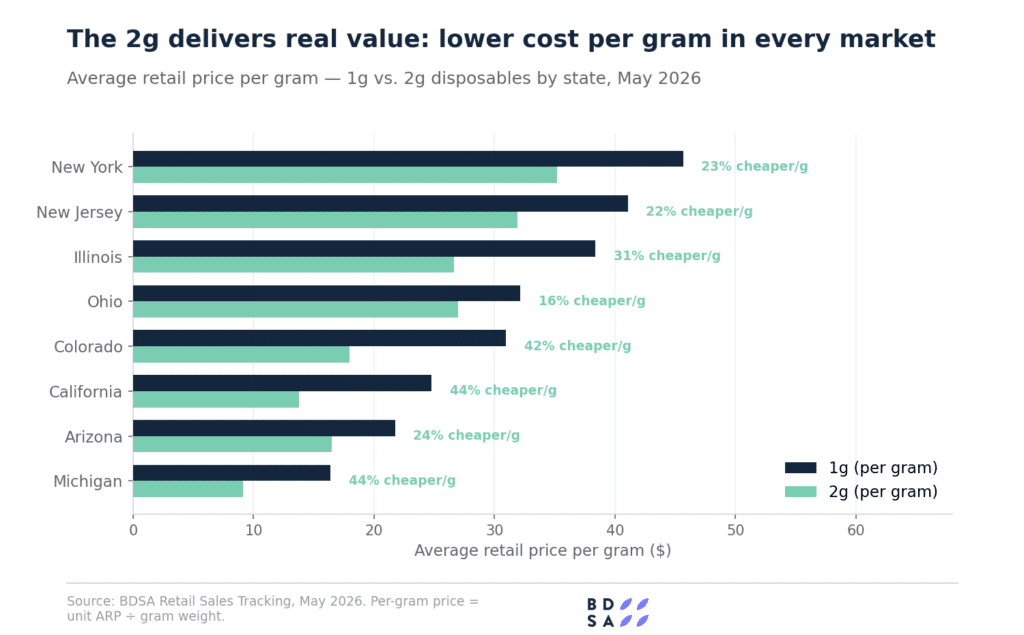

Why are 2-gram disposables growing so fast? The economics work for both sides of the transaction. For brands and retailers, the larger format commands a higher shelf price, generating roughly 30% more margin dollars per unit sold at nearly identical margin percentages (though it’s worth noting this also does vary greatly state-by-state). For consumers, a 2g disposable lasts longer, reduces the need to recharge or repurchase, and delivers genuinely better value per gram — 34% more cannabis for their dollar.

California is a notable exception. 2-gram disposables are not currently permitted in the state, which explains their complete absence from the largest cannabis market in the country. If that regulatory position changes, the national 2g trend would likely accelerate significantly.

Which brands are leading in 2-gram disposables? Select runs 86% of its disposable business through the 2g format and leads in raw 2g dollar volume nationally. Dime Industries, Fernway, &Shine, Savvy, and Rythm all run 60% or more of their disposable mix through 2g. Interested in more information about the top brands driving sales? Top 10 Vape Brand Blog.

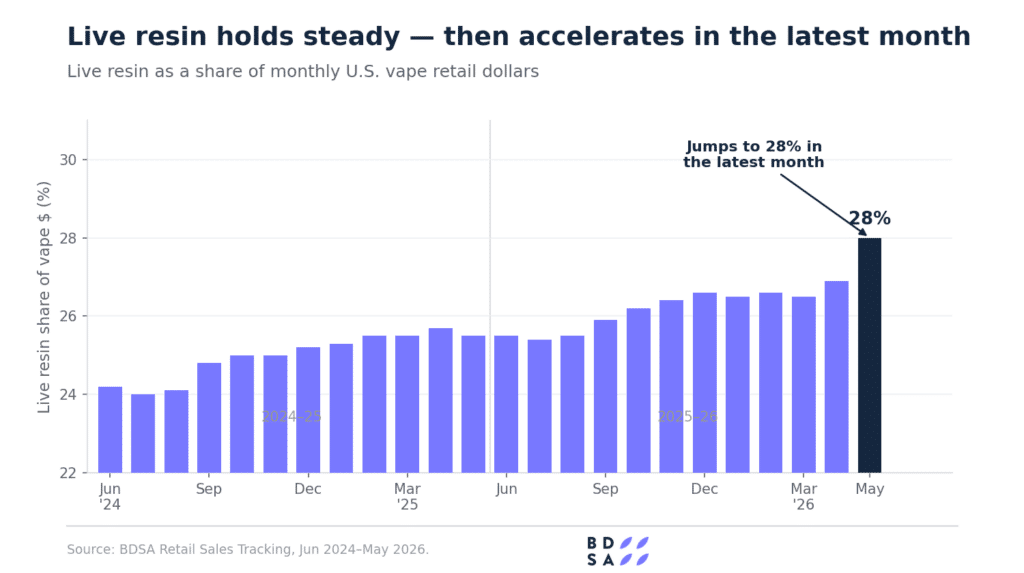

4. Live resin vape is gaining share — and rosin is building a loyal base

The short answer: Premium oil formats, live resin and rosin combined, now account for 32% of U.S. vape sales, up from 28% a year ago. Live resin is actively gaining share; rosin has found a stable, growing niche.

Live resin and rosin together accounted for 32% of vape revenue over the past 12 months, up from 28% the prior year. But the two formats are telling different stories within that number.

Live resin vape is the format actively gaining share. It reached $2.1 billion in the past 12 months, representing 26% of total vape sales. Its share held a steady plateau near 26% for most of the year, then jumped to 28% in May 2026. That acceleration in the most recent month is the clearest signal that premiumization is speeding up rather than plateauing.

Rosin vape is smaller but stable and growing. At roughly $442 million over the past 12 months, rosin represents about 5.5% of the vape market — a share it has held consistently every month over the past year. Dollar growth is healthy at around 19% year over year. Rosin has found a settled consumer base among consumers who prioritize solventless extraction, without yet breaking into the mainstream the way live resin has.

Distillate vape, meanwhile, is losing share while staying roughly flat in absolute dollars — falling from about 59% of vape on a trailing basis to 55% in the most recent month. The category is not abandoning distillate; growth is simply concentrating at the premium end.

5. Cannabis vape brand consolidation: what is actually happening?

The short answer: The national vape brand count is essentially flat month-to-month, but that stability masks two opposite trends — new markets adding brands rapidly while mature markets consolidate significantly.

The trailing-12-month brand count fell 17%, from roughly 6,600 to 5,500 — a loss of more than 1,100 brands. But the single-month active brand count tells a different story: roughly 4,225 vape brands recorded sales in May 2026, slightly more than the 4,106 active in May 2025. Both numbers are true. They are measuring different things.

Why is the trailing-year brand count falling while the monthly count is flat? New and expanding markets are adding brands rapidly, offsetting consolidation already underway in the most mature states.

New and expanding markets (brand counts rising):

- Minnesota launched adult-use retail in September 2025; its vape brand count has nearly quintupled since

- New York, still in active retail expansion, added more than 60 new vape brands year over year and now has over 330 active in a single month

Mature markets (brand counts declining):

California, Pennsylvania, Oklahoma, Michigan, Colorado, Ohio, Arizona, and Massachusetts all had fewer active vape brands in May 2026 than in May 2025. California and Pennsylvania illustrate the pattern most clearly: both shed brands in double-digit percentages year over year while simultaneously growing vape sales — California up 16%, Pennsylvania up 4%. Fewer brands competing for more dollars is the defining characteristic of a consolidating market, and it is already the reality in the states that have been open longest.

The national consolidation story is real but concentrated in mature markets, and largely invisible in the headline number because new-market expansion is refilling the pool. As markets like New York and Minnesota mature and their brand counts peak, the national figure will start to reflect what the mature markets are already showing.

What the 2026 cannabis vape trends mean for brands, retailers, and investors

The vape category’s stable top line hides a remarkable amount of structural change — and most of it is recent:

- Disposables crossed 50% of the format mix for the first time in April 2026

- The 2-gram disposable doubled its share in two years and is now 35% of all disposable dollars

- Live resin reached its highest share of the year in May 2026 at 28%

- Vape surpassed flower in California and Washington

- Mature markets are losing brands while growing dollars — the textbook definition of consolidation

For brands, retailers, and investors, one practical implication is about measurement: in a category moving this quickly, trailing-12-month benchmarks can describe a market that no longer exists. The trends most important to watch are not the ones that have already played out in the annual numbers. They are the ones showing up in the most recent month, state-by-state.